Alfredo Carrillo Obregon and Clark Packard

Last week, President Trump announced the United States was imposing a 50 percent “national security” tariff on copper imports. Details are sparse, but Bloomberg reported that it will include all refined copper and semi-finished goods (i.e., bars, rods, wires, plates, etc.). As 60 years of failed steel protectionism—including the last seven-plus years of “national security” tariffs on imported steel and steel derivatives—demonstrate, new copper tariffs are unlikely to reshore much copper production anytime soon, but will surely cause enormous pain in the ensuing years.

First, a little background. From plumbing and electrical wiring to automobiles and aircraft, copper is a critical input for numerous products and industries. Last year, copper and copper alloy (i.e., mixtures of copper with other elements) products were used in construction (42 percent of total consumption), manufacturing of electrical and electronic products manufacturing (23 percent), transportation equipment (18 percent), consumer and general products (10 percent), and industrial machinery and equipment (7 percent). Of the estimated 1.6 million metric tons (MMt) of refined copper consumed by Americans in 2024, approximately half (810,000 MMt) was imported.

So, how easily could these imports be replaced? Data from Benchmark Mineral Intelligence suggests that US production of mined and scrap copper (i.e., copper obtained from recycled products) is sufficient to meet domestic demand. But there’s a catch: the United States lacks the refining and smelting capacity to transform copper ore and copper scrap into refined copper. Indeed, S&P Global indicates that whereas US copper mining capacity has grown from 1.7 MMt in 2000 to 2.1 MMT in 2024, US refining capacity has declined in that same period.

This mismatch between mining/recycling and the smelting/refining is further borne out in the trade data: Whereas the United States is a net exporter of copper ores and concentrate and of copper scrap, it is a net importer of refined and semi-finished copper.

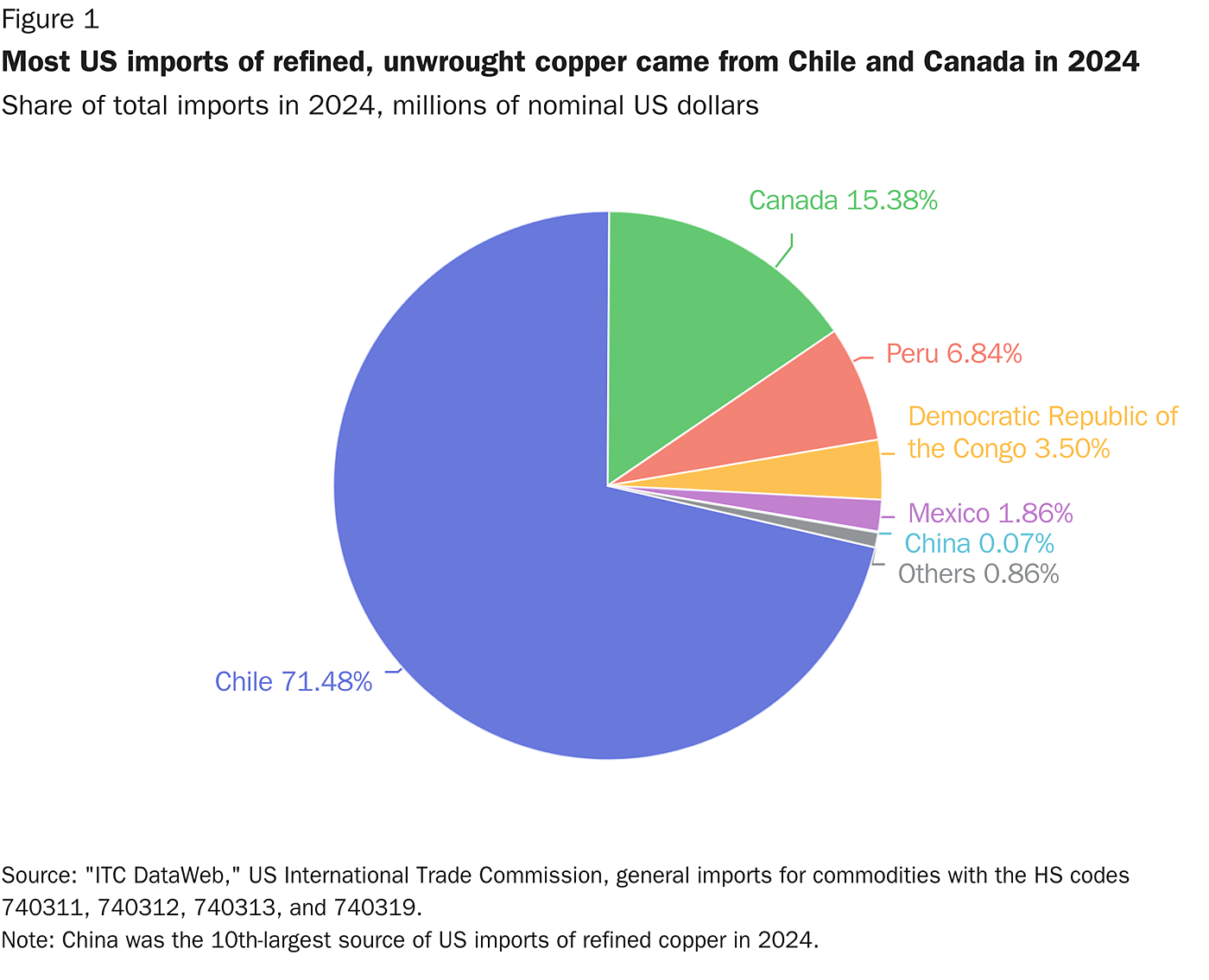

Looking at these product categories, the main sources of imported refined copper are, overwhelmingly, Chile and Canada, with Peru, the Democratic Republic of the Congo, and Mexico rounding up the top five (Figure 1). For all of President Trump’s talk about national security, none of these countries can be considered US adversaries. On the contrary, the United States has free trade agreements with four of them. (The DRC, the lone exception, is covered by the African Growth and Opportunity Act that provides duty-free access to the US market for over 1,800 products.)

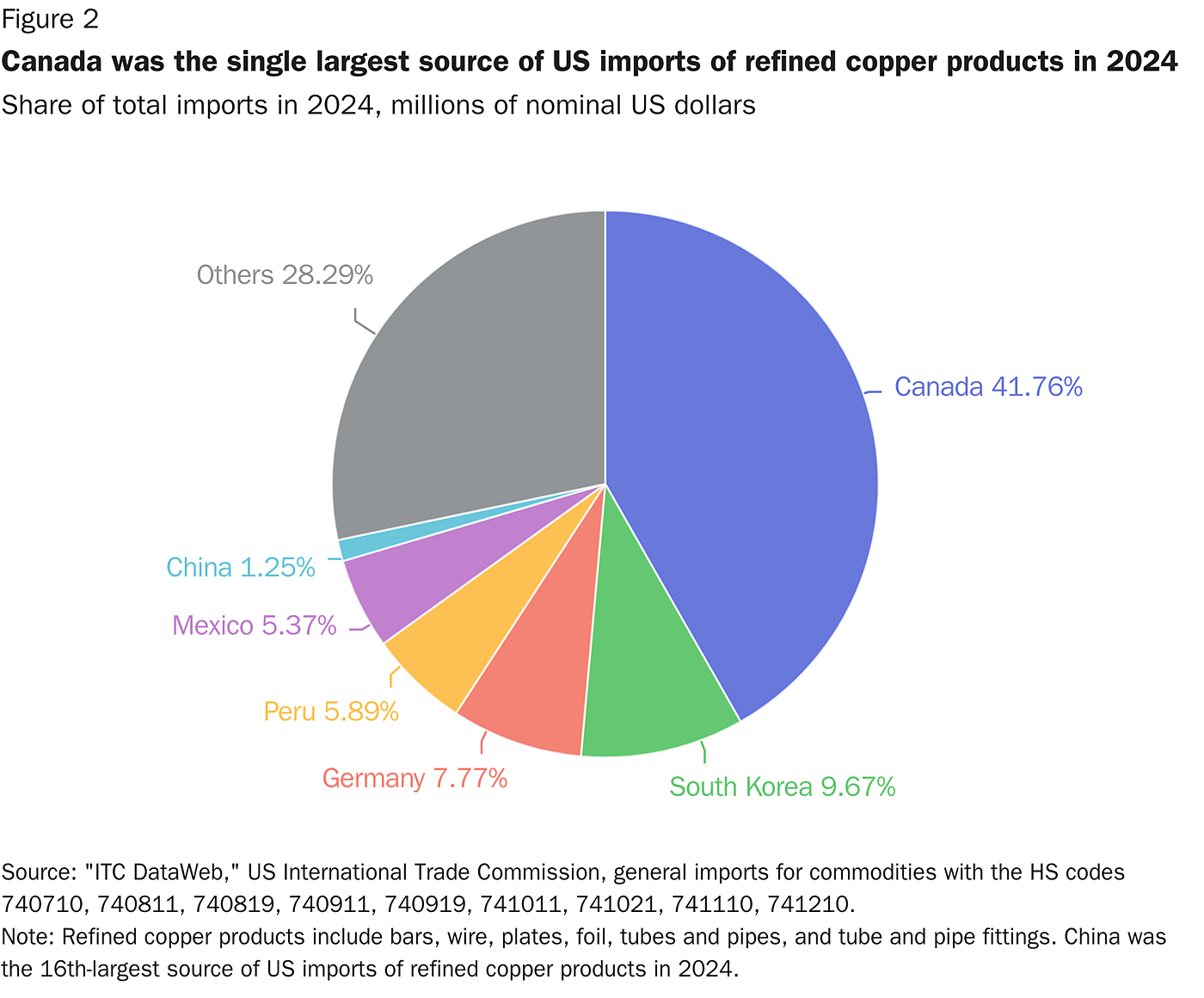

Regarding semi-finished copper, meanwhile, the main US import sources are similarly uncontroversial, with Canada supplying most of the bars, rods, wires, and other products made from refined copper, and countries such as South Korea, Germany, Peru, and Mexico also being important sources (Figure 2). (The data bear similar results for both unwrought and semi-finished copper alloys.)[1]

Such sourcing hardly suggests a national security threat that justifies tariffs under Section 232.

Similarly, claims that the tariffs are designed to address China’s global preeminence in copper smelting and refining, as well as Chinese-driven global copper overcapacity and Chinese “control” of global copper supply chains, are also questionable.

Although China certainly accounted for a large share (about 45 percent) of global copper refinery production in 2024, and Chinese smelting overcapacity has created distortions within the country and in global markets (to the point that Beijing has enacted policies to curb further capacity expansion in the sector), US imports of refined copper come mainly from longstanding trusted trading partners. In 2024, China accounted for less than 1 percent of total US imports. Even in the case of US imports of semi-finished articles made of refined copper, China only accounted for 1 percent of the total.

If the goal is to curb Chinese overcapacity, these new tariffs are hardly a means for addressing the issue.

But the enthusiasm for tariffs despite such facts shouldn’t surprise. Previous Section 232 invocations (i.e., steel and aluminum, autos and auto parts) and the general conduct of US trade policy under the Trump administration strongly indicate that the identity of our trading partners matters little to a president with long-held protectionist views. As our colleague Scott Lincicome has pointed out, he just really likes tariffs.

But beyond the questionable nature of the alleged threat, there are strong reasons to doubt that tariffs offer a solution, even if one accepts the premise that expanded domestic refining and smelting capacity and a stronger overall copper industry are needed.

Instead of imposing fresh tariffs, the White House’s energy would be better spent tackling domestic policy issues that inhibit the US copper industry from adding more capacity. As the Wall Street Journal points out, building and permitting a copper smelter in the United States can take more than five years. A public submission to the Bureau of Industry and Security from Asarco, which is trying to reactivate a smelter in Hayden, Arizona, shuttered since 2019, claims that stringent environmental regulations and the methods for enforcing them have led to a lack of investment in the facility.

Such onerous regulatory burdens perhaps help explain why there are only five US copper refineries, down from nine in 2000, and only two primary copper smelters.

There are similar issues in copper mining. According to S&P Global, it takes an average of 29 years for a mine in the United States to begin production after mineral deposits are discovered, the second-longest timeline in the world behind only Zambia, due to the lengthy permitting process (about seven to 10 years, per ING). And while developing mines in other Western countries, such as Canada and Australia, can also take a long time (27 and 20 years, respectively) US-based projects also suffer from comparatively less certainty that they may ultimately reach the production stage, as well as a higher risk of litigation. Resolution Copper offers a case in point. Although a promising mine in Arizona that could supply up to a quarter of current US copper consumption, it has been stuck in the permitting process since 2013 and mired in litigation. Tackling such red tape would be a far better use of the administration’s time than imposing new import taxes on Americans.

Recent experience with the Section 232 steel and aluminum tariffs provides additional cause for concern: though the tariffs have been in place for more than seven years, both steel production and capacity utilization are below the level they were when the tariffs were first imposed. Meanwhile, as a plethora of studies have documented, those tariffs created large costs for the numerous US industries that consume steel.

Copper tariffs are likely to have a similar impact. Indeed, the cost to US consumers could be perhaps even larger due to a) comparatively higher US reliance on refined copper imports (45 percent of apparent domestic consumption in 2024) than on finished steel mill imports (13 percent of apparent domestic consumption in 2024) and b) an inability to quickly ramp up domestic copper production.

In the months following the Section 232 investigation’s announcement in February 2025, copper imports exploded, driven by imports of refined copper (Figure 3), and inventories at US-based COMEX warehouses similarly expanded significantly over the same period. That should provide some cushion against near-term price increases. But the tariff bill must eventually come due, and the price of COMEX copper futures soared shortly after President Trump’s announcement of a 50 percent tariff.

If the cost of these tariffs is passed through to consumers—as occurred with the steel and aluminum duties—the consequences for US businesses and consumers could be dire, particularly given the ubiquitousness of copper in everyday life. The costs could further compound if the administration also extends the tariffs to cover derivatives (as it did with steel tariffs), which certain industry representatives advocated for in a submission to the Bureau of Industry and Security.

Altogether, both the reality of the domestic US copper industry and our fraught experience with other Section 232 duties, particularly those on steel, should caution that a 50 percent tariff on copper is unlikely to produce much reshoring of lost refining and smelting capacity or ramped-up mining of this essential mineral. Meanwhile, recent experience suggests the tariff is likely to increase prices for copper consumers, inflict damage on the US economy, further strain already-tense relationships with longstanding allies and trading partners, and foment additional political dysfunction at home.

Despite its already extensive experience with the downside of metals’ tariffs, there are some lessons the Trump administration unfortunately seems unwilling to learn.

[1] China did account for 12 percent of US imports of semi-finished copper alloy products in 2024, the value of these imports ($230 million) is only a fraction of total US imports of semi-finished copper products ($6.9 billion).